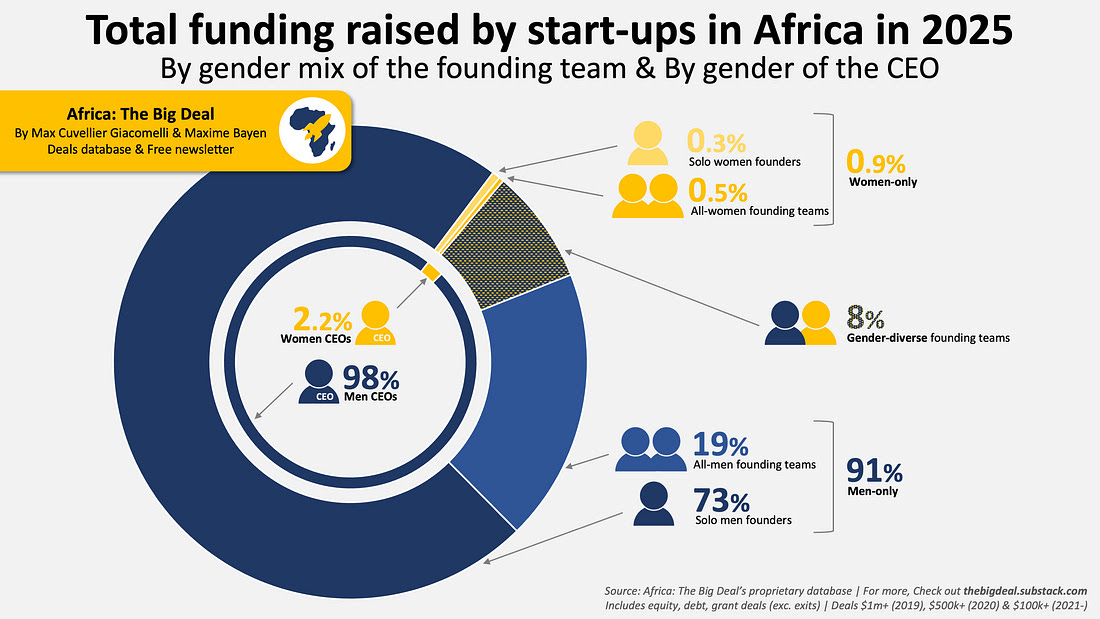

African Fintech sector has retained its position at the top of the continent’s funding table in 2025, even as the broader market reshapes around a handful of very large deals.

According to reports by Africa:The Big Deal, after falling sharply from $3bn in 2023 to $2.2bn in 2024, total startup funding on the continent rebounded to $3.2bn in 2025.

However, the recovery was not driven by a surge in the number of companies raising capital. Instead, the number of startups securing $100k+ remained broadly stable.

In fact, 2025 was powered by a small group of sizeable cheques and debt facilities, rather than a broad expansion of smaller tickets.

Financial technology: Still number one, but narrower

Fintech remained the largest sector by capital raised. It pulled in $1.2bn in 2025, slightly up from $1.1bn in 2024, across 124 companies, a drop in participation compared with the previous year.

Yet, while fintech kept its crown, it did not broaden.

Concentration at the top eased slightly. In 2025, the top five fintech raisers — M-Kopa, Wave, MNT-Halan, Moniepoint and ValU — accounted for $607m (52%) of the sector’s total.

“That compares with $618m (58%) in 2024 and 66% in 2023.”

The report further states that equity continued to do most of the heavy lifting at $685m. However, debt played an outsized role, contributing $467m and helping to keep the overall figures high despite fewer funded companies.

Wave’s $137m debt facility and MNT-Halan’s bond issuance illustrate how single transactions can materially shift sector totals.

Meanwhile, exits also picked up. In 2025, the continent recorded 49 exits, more than double the 22 recorded in 2024. Fintech accounted for 19 of those, underlining the sector’s maturity relative to others.

Renewable energy industry: Debt-driven surge reshapes the field

If fintech showed continuity, energy marked a structural shift.

The sector raised $857m across 50 companies in 2025 — a sharp rebound from $445m in 2024, and roughly back to its 2023 level of $792m.

However, concentration intensified. The top five energy companies captured $701m (82%) of the total in 2025, up from $351m (79%) in 2024, and 75% in 2023.

Debt was the principal driver. Of the sector’s $857m, some $611m (71%) came via debt financing — and it was heavily stacked.

d.light secured $300m, while Sun King raised $156m. Other large facilities, such as BURN Manufacturing’s $80m, reinforced the pattern.

As a result, energy now looks structurally different from many other sectors: a small cluster of very large, predominantly debt-led transactions is pulling overall totals upwards.

Outside fintech and energy, the picture shifts.

Logistics industry & Transport raised $309m across 63 companies, and was overwhelmingly equity-led, with 87% of funding coming through equity.

Healthcare industry attracted $211m across 49 companies. Again, equity dominated. Yet one deal did much of the work: LXE Hearing’s $100m round alone represented roughly 47% of the sector’s total.

Meanwhile, Agriculture industry & Food ranked lower on capital raised at $122m, but stood out for breadth, with 62 companies securing funding.

Climate Tech: A theme gaining ground

One cross-cutting theme that continues to grow is climate tech.

Not a sector in itself, climate tech spans energy, agriculture, logistics and beyond. In 2025, climate-focused startups raised $1.2bn across 149 companies, accounting for 38% of total funding.

That compares with $761m (34%) in 2024, and $1.1bn (38%) in 2023.

Importantly, participation is rising. Climate tech companies represented 26% of funded startups in 2023, 28% in 2024, and 29% in 2025. By contrast, in 2021–2022, the share was closer to 18–20%.

In other words, climate tech is one of the few themes combining scale with steadily expanding breadth.

Taken together, 2025’s figures suggest recovery — but not uniform expansion.

Total funding has returned to $3.2bn, yet the market remains shaped by concentration: large debt facilities in energy, and a handful of dominant fintech players, continue to drive the numbers.

Therefore, while the headline rebound is clear, the underlying structure tells a more nuanced story — one of selective growth, rising climate focus, and an ecosystem still reliant on big-ticket capital to move the needle.